Trade and geopolitics

ASEAN is a destination of choice for investment – but must act as one

Published 05 August 2025

ASEAN has a rare moment of strategic opportunity. When much of the world is fragmenting, Southeast Asia is emerging as a draw for foreign capital as an open, neutral, and connected region, but structural friction continues to chip away at its potential. Robin Hu, Asia Chairman of the Milken Institute and Temasek’s Advisor Senior Director, writes on the need for ASEAN to move from promise to performance before its historic window narrows.

Amid a global wave of decoupling, reshoring, and strategic hedging, the Association of Southeast Asian Nations (ASEAN) has emerged as a rare zone of opportunity: an open, neutral, and connected region at a time when much of the world is fragmenting. It is drawing serious capital, not because it has achieved seamless integration, but because it offers something investors now prize above all: trust, optionality, and relative stability.

Foreign direct investment (FDI) into Southeast Asia surged to US$224 billion in 2022, up more than 40% from the year before. Vietnam, Indonesia, and Malaysia are among the top beneficiaries of this shift in capital allocation, while Singapore remains a financial, digital, and logistics hub of regional gravity.

That investors are committing capital despite ASEAN’s still fragmented FDI policy architecture speaks volumes. But this vote of confidence should not breed complacency. ASEAN’s structural friction — non-tariff barriers, regulatory divergence, political divergence — continues to chip away at its potential. What is missing is not demand, but cohesion and scale. ASEAN must now demonstrate whether it can move from promise to performance before this historic window narrows.

Related Article

A platform of promise, still disjointed

The ASEAN Economic Community (AEC), launched in 2015, was founded on a bold vision: a single production base, enabled by the free movement of goods, services, capital, and skilled labor. But in practice, progress has lagged.

Tariffs have largely been eliminated, but non-tariff barriers persist. Licensing bottlenecks, inconsistent product standards, and duplicative customs procedures continue to weigh down intra-regional trade. In 2023, intra-ASEAN trade accounted for just 22% of total trade, unchanged from a decade ago.

ASEAN’s diversity is part of its appeal, but also a source of inertia. Varied political systems, economic development gaps, and a deep-seated reluctance to cede sovereignty have rendered its institutions relatively weak. Initiatives such as the ASEAN Power Grid and the Singapore–Kunming Rail Link remain mired in bilateral implementation rather than regional momentum.

And yet, the region continues to attract capital. Why?

Neutrality in a divided world

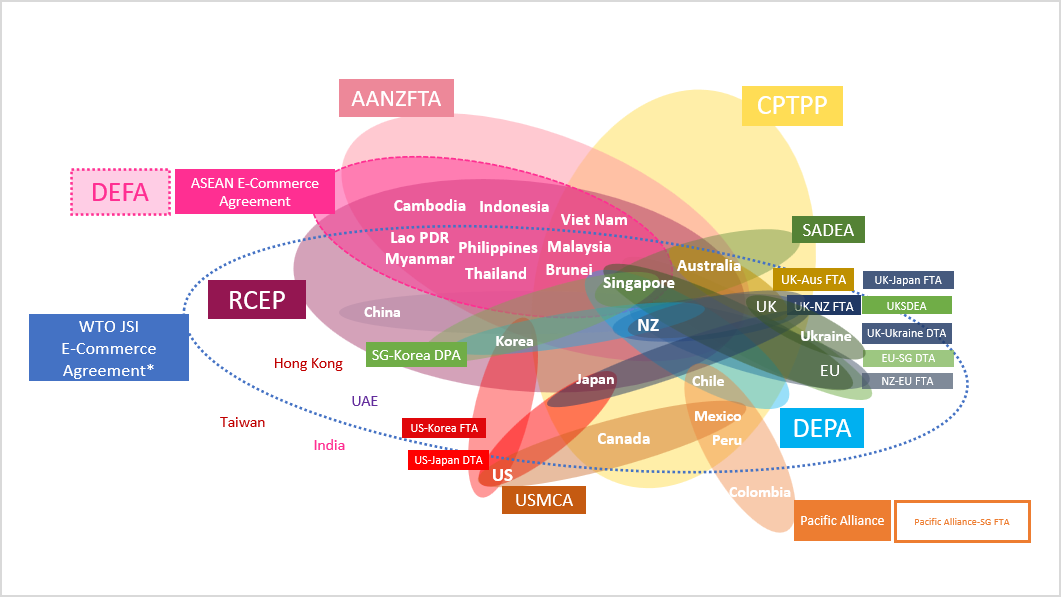

In a world fractured by US-China rivalry, tariff wars, and diverging standards, ASEAN offers geopolitical neutrality and strategic optionality. The region’s non-aligned posture, coupled with overlapping trade frameworks like Regional Comprehensive Economic Partnership (RCEP) and Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), provide firms with a base for connectivity, diversification, and risk mitigation.

This appeal is not limited to the larger economies. Smaller ones such as Cambodia and Laos are benefiting from infrastructure spillovers linked to China’s Belt and Road Initiative. Brunei is tapping into halal logistics and energy corridors. Timor-Leste’s accession to ASEAN, expected to be formalized in October 2025, opens new conversations about developmental potential.

But for ASEAN to remain relevant, it must resist the drift toward strategic fragmentation. While the bloc speaks with one voice in multilateral settings, member-states are quietly diverging. In private conversations, officials from Vietnam, Malaysia, the Philippines, and Thailand acknowledge their efforts to court Chinese capital, particularly for infrastructure and manufacturing, but express growing unease.

Related Article

They are wary of China’s expansive maritime claims, its assertive diplomacy, and the conduct of some Chinese firms. These Chinese companies often operate in insulated ecosystems, bringing in their own workers, bypassing local supply chains, and skirting labor or environmental standards. Compared to G7 investors, the local economic multipliers are often shallower.

This quiet hedging makes regional alignment more urgent. ASEAN’s bargaining power depends not only on market size, but on whether it can present a coherent front.

Reforms are within reach

The good news: reform is not a fantasy. It is feasible and long overdue.

Digitized customs platforms, mutual recognition of professional qualifications, and harmonized food and pharmaceutical standards are all achievable in the near term. Infrastructure integration like rail, energy grids, and digital payments can be accelerated with blended finance and political will.

Singapore’s Prime Minister Lawrence Wong was right when he called for "bolder ASEAN reforms" at this year’s Summer Davos, officially known as the Annual Meeting of New Champions organized by the World Economic Forum. Even modest steps toward interoperability would unlock substantial efficiency gains across borders.

Related Article

The role of private capital

Governments have a role to play in setting the enabling framework. But private capital must take the lead in solving practical bottlenecks.

Private equity and venture capital are already backing firms that enable cross-border logistics, digital payments, and small and medium-sized enterprises’ (SME) financing. Take the example of Grab, which had to build a multi-market payment and regulatory stack from scratch. Or logistics platforms like Ninja Van and Lalamove, which are now helping to streamline last-mile delivery across ASEAN’s fragmented borders.

These are not just growth stories; they are system-level solutions. Investors who combine capital with operational know-how and strong local partnerships can help build the connective tissue ASEAN needs.

Volatility and value discovery

Recent political developments are a mixed bag. Instability in Thailand and shifting priorities in the Philippines raise governance questions. Border tensions between Cambodia and Thailand, and Myanmar’s internal crisis, add complexity. Divergent foreign policy stances, from Vietnam’s hedging posture to Cambodia’s close alignment with China, challenge regional unity.

But these are not reasons for exit. They are reasons for precision. In complexity lies opportunity, especially for long-term capital capable of navigating local nuance. Country risk premiums may be elevated, but so too is the potential for mispricing.

Related Article

What remains undisputed is ASEAN’s structural appeal. The region is home to more than 660 million people, with a median age under 30. Its digital economy is projected to reach US$1 trillion by 2030. Consumption is rising. Urbanization continues. Fintech, healthtech, and green infrastructure are gaining ground.

Act as one or be bypassed

ASEAN does not need to be perfect to succeed. But it does need to be coordinated.

Investors want ASEAN to thrive. But investors need more than ambition from ASEAN. They need consistency, interoperability, predictability, and scale. Being "open for business" is not enough. ASEAN must act as one if it hopes to compete as one.

It’s not a question of whether ASEAN is investable. The real question is whether we’ve recognized that ASEAN’s unity is essential.

This is a moment of strategic opportunity. But it is also a moment that can be lost. The world is watching, capital included.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Robin Hu

Robin Hu is Asia Chairman of the global think tank Milken Institute. He is also an Advisor Senior Director at the Singapore government-owned global investment firm Temasek International.

Have any feedback on this article?

Related Articles

Trending Topics

BACK TO TOP