Sustainable trade

OECD Inventory of Export Restrictions on Industrial Raw Materials 2025

Published 24 June 2025

As technologies develop, geopolitical tensions flare, and demand for key materials grows, economies are increasingly regulating access to inputs critical for cutting-edge production. The latest edition of the OECD’s Inventory of Export Restrictions on Industrial Raw Materials examines what restrictions economies are imposing and why. Explore our analysis of the OECD Inventory of Export Restrictions on Industrial Raw Materials 2025.

Here’s how to use the OECD report titled Monitoring the Use of Export Restrictions Amid Growing Market and Policy Tensions May 2025.

Why is the OECD Inventory important?

The Inventory was published at an especially relevant moment, as China used export controls over critical minerals necessary to industrial production to gain leverage over the US and other trading partners at a key period of intense trade negotiations. Monitoring the use and evolution of export restrictions on such important industrial inputs is vital for understanding where supply chain chokeholds are likely to occur, and for considering how to address trade flows and rules governing them in the future.

What’s in the OECD Inventory?

The Inventory includes three principal sections:

- International trade in industrial raw materials and export restrictions;

- Key trends in the use of export restrictions up to 2023; and

- Implications.

Section 4 of the Inventory, About the OECD Inventory on Export Restrictions on Industrial Raw Materials, describes its data sources collection process, products and countries covered, and kinds of measures covered, noting the OECD’s goal of improving transparency and building a databased of border and domestic measures that restrict the export of industrial raw materials. (pp. 17-20, Tables 4.1-4.3)

International trade in industrial raw materials and export restrictions

- From 2009-2023, export restrictions on industrial raw materials increased more than fivefold, accelerating in 2023 with the war in Ukraine; seven countries – China, Vietnam, Burundi, Russia, the DRC, Zimbabwe, and Laos – accounted for 94% of new restrictions; restrictions risk disrupting supply chains so understanding their impact is necessary to find less restrictive alternatives. (p. 4)

- Minerals are essential to security and prosperity, critical to renewable energy, digitalization, and defense, and vital to semiconductors, fibre optics, superalloys, permanent magnets, and advanced electronics; mineral extraction and processing are highly concentrated geographically and in ownership, with the top three producing countries accounting for over two-thirds of global production of cobalt and nickel and over 90% of rate earth elements and lithium, with China along producing 70% of the world’s supply of germanium, graphite, rare earths, and magnesium. (p. 4)

- The concentration of production, combined with rising demand, geopolitical tensions and strategic rivalries, intensifies pressure on trade of raw materials, leading to more assertive management of raw materials by governments; export restrictions take many forms and pursue diverse objectives, however, the effectiveness of such restrictions in achieving sustainable development goals is contested, and restrictions by one country often trigger similar actions by others and a cycle of rising prices and reduced global supply; the sharp increase in restrictions in 2023 may mark the start of a new phase in how countries manage critical raw materials. (p. 5)

How to apply the insights

-

This section provides a quick summary of the current state of play on the importance of critical raw materials and the tensions driving new restrictions, as well as flagging that 2023 may have marked a turning point for restrictions.

-

This is a useful section for anyone seeking a general overview.

Key trends in the use of export restrictions up to 2023

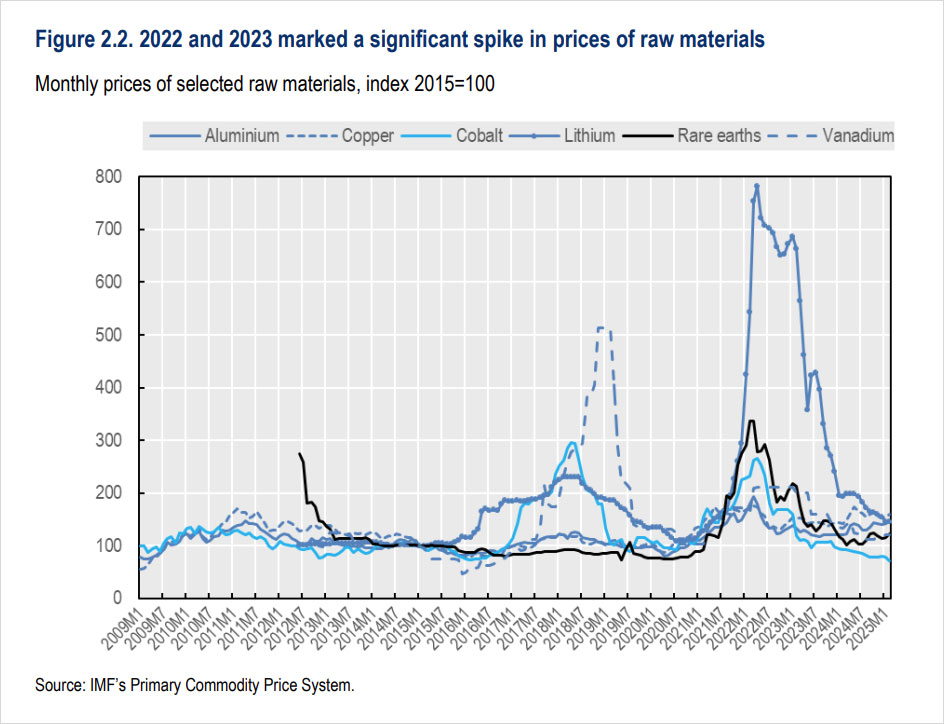

- In 2023 the pace of use of export restrictions accelerated; by the end of 2023 approximately 3.4% more raw material products were subject to at least one export restriction compared to 2022, more than double the rate of 2022 and triple the rate of 2023, coinciding with the rise in energy and raw material prices following Russia’s invasion of Ukraine and a period of rising geopolitical tensions. (pp. 6-7, Figures 2.1-2.2)

- Most of the new export restrictions imposed by China, Vietnam, Burundi, and Russia were new taxes or revised tax rates; the DRC and Zimbabwe adopted export prohibitions to promote local processing; several raw materials saw a global increase in export restrictions incidence of more than 10%, particularly magnesium, mercury, arsenic, and boron. (pp. 7-9, Figures 2.3-2.4)

- By 2023’s end, waste and scrap products faced the highest incidence of export restrictions, reflecting environmental concerns over the export of such materials for disposal and the desire to leverage the circular economy as a source of supply for certain metals and minerals; restrictions on ores and minerals increased more rapidly than other segments and nearly twice as fast as the overall average for all restrictions, corresponding to the high and rising concentration of production, imports, and exports in the upstream part of the supply chain and aligning with the policy of supporting domestic downstream industries. (pp. 8-9, Figure 2.5)

- Molybdenum, potash, tungsten, zirconium, and germanium had some of the steepest increases in export restrictions; manganese, titanium, zirconium, germanium, coppers and other non-ferrous metals recorded the highest overall levels of export restriction incidence in 2023; between 2021 and 2023, approximately 14% of global trade in non-waste and scrap industrial raw materials was subject to at least one export restriction and more than 20% of global exports of cobalt, rare earth elements, tin, palladium, and other previous metal ores faced at least one export restriction; 67% of cobalt and 46% of rare earth elements faced at least one export restriction. (pp. 10-11, Figures 2.6-2.7)

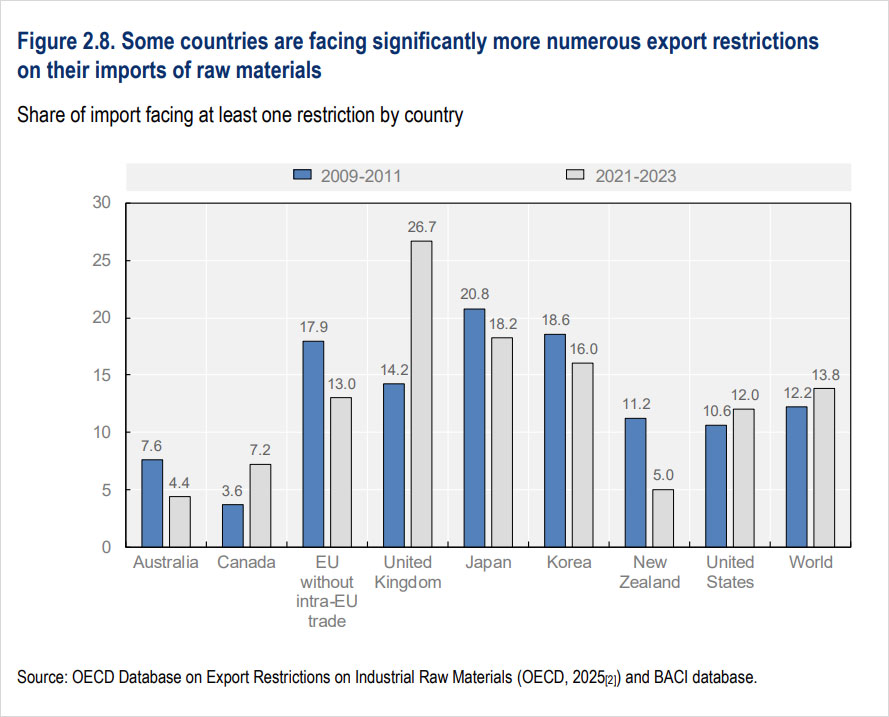

- Some countries face significantly more export restrictions than others, increasing due to a growing concentration of imports subject to relatively high levels of export restrictions and a rising incidence of restrictions on existing flows; decreases result from a shift away from trade flows with high restrictions incidence and a decline in restrictions affecting existing flows; China, India, Vietnam, Argentina, and Burundi were the top five countries in terms of new export restrictions introduced between 2009 and 2023. (pp. 12-13, Figures 2.8-2.9)

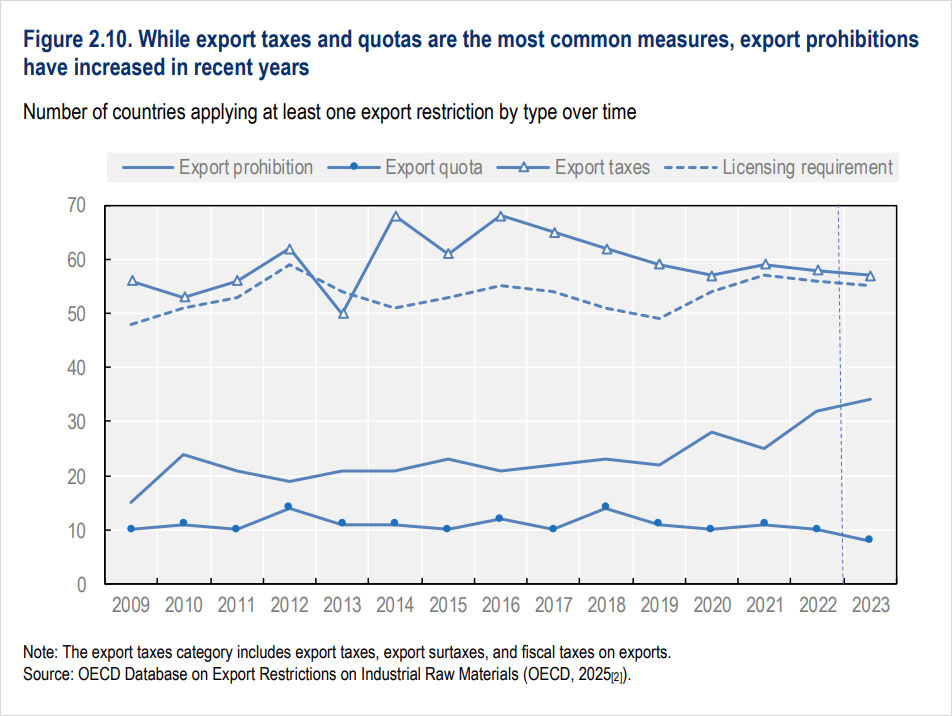

- Export taxes and licensing requirements contributed the most to the growth of export restrictions between 2009 and 2023; under WTO rules, quantitative export restrictions are generally prohibited but export taxes and licensing requirements are not, however, the use of quantitative export restrictions like export prohibitions and quotas has been on the rise in recent years with the most restrictive, export prohibitions, increasing significantly since 2019; revenue generation is the most frequently cited justification, with safeguarding domestic supply, promoting further processing or value-add, and protecting local downstream industries growing in importance; in 2023 export restrictions were justified under the need to monitor and control export activity including conservation of natural resources. (pp. 12-15, Figures 2.10-2.12)

Implications

- Given the global economy’s high interdependency and many countries’ reliance on international trade for critical raw materials, export restrictions risk negative spillover effects across global supply chains, highlighting the need for co-operative solutions to limit such measures; understanding the motivations behind export restrictions and their impact on trading partners and global markets is crucial to help identify less restrictive ways to meet both the security of supply needs of importing countries and the development goals of resource-rich nations. (p. 16)

How to apply the insights of the above two sections

-

This section is the key to the Inventory’s analysis, presenting how export restrictions have grown in recent years, where, what products are affected, the restrictions applied, and the implications of these policy evolutions.

-

These trends are vital for policymakers to track as geopolitical tensions and demand for these materials increase.

Conclusion

The OECD Inventory comes at a crucial moment for trade in critical minerals, providing the current state of play and important trends to watch as restrictions evolve and demand grows for vital industrial inputs.

Complementary reports and analysis

Hinrich Foundation

- Can Trump break China’s critical minerals stranglehold?

- China’s long shadow on critical minerals looms over Asia

- The real cost of export restrictions

External Resources

-

How export restrictions threaten economic security – Peterson Institute for International Economics

PIIE analyzes recent examples of export restrictions, considering how these restrictions and the fear of them lead to the adoption of industrial policy initiatives to build resilience in supply chains, and the importance of international cooperation on trade and industrial policy. -

WTO Report on G20 Trade Measures – WTO

The WTO presents actions taken by G20 economies on trade over the course of a year, giving a strong indication of how trade flows and policies are changing, and how trade will evolve in the coming year. -

Raw materials critical for the green transition - OECD

The OECD defines raw materials critical for the green transition, and where, how, and to what extent these materials are concentrated in terms of production and trade, examining which economies show high dependencies on others for these resources.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).