Trade and geopolitics

Australia’s rare earths lie between economic security and liberal markets

Published 24 June 2025

Australia’s rare earths are becoming a case study for whether liberal market economies can successfully implement economic security and industrial policy in our new geoeconomic world order. Canberra has taken steps to reduce exposure to the global dependence on China’s near-monopoly on these and other critical minerals. But for these efforts to pay off, policymakers will have to wholly reconceptualize the way market-driven commercial ecosystems work.

Beijing has turned China’s dominance in critical minerals, built on a formidable mix of economic scale advantages and industrial policy foresight, into a key tool for responding to strategic pressure from Washington. In response, Western governments have developed a splurge of security-of supply policies, ranging from self-sufficiency to friend-shoring. The hurdles to break Beijing’s critical minerals monopoly remain high, but as the geopolitical need grows, opportunity beckons.

Australia is laying the grounds to position itself as an alternative supplier of China in rare earth elements (REEs), the group of critical minerals indispensable to high-tech manufacturing where Beijing’s dominance is greatest. Key to Canberra’s success will be the effective transition from a global mining powerhouse to a mining-to-refining powerhouse, first mapped out in the federal government’s 2019 ‘Australia’s Critical Minerals Strategy’. The report signifies Australia’s recognition that the state has a new role to play in market formation in strategic sectors where market advantages are insufficient to compete with state-backed supply.

Download Australia’s rare earths lie between economic security and liberal markets by Naoise McDonagh:

Critical dilemma: China’s strategic foresight

China accounts for 60% of global rare earth element mining output, and almost 90% of processing. Given the level of processing dominance, even the balance of non-Chinese unprocessed REE mining output is dependent on China as a buyer to feed the country’s vast downstream ecosystem. This means China holds both monopsony power (over non-China ore supply) and monopoly power (over processed output). REEs are crucial to technology supply chains as inputs to defense sector goods, advanced consumer electronics, as well as crucial components of the permanent magnets powering global electrification. China controls a staggering 90% of the world production of standard and high-temperature-operation neodymium-iron-boron (NdFeB) magnets. The remaining 10% of ex-China magnet supply is heavily dependent on China for raw material inputs.

Given that rare earth elements are far from geologically rare, it is the highly technical, environmentally polluting, and complex metallurgy of the processing phase that is the major barrier to supply diversification. Rare earths can have up to 1,000 chemical stages from ore through to final metal. Chinese state-owned or state-backed firms’ long-term operation and China’s focused R&D efforts on processing means Chinese firms hold world-leading intellectual property and trade secrets underlying cost-effective REE processing.

A further challenge for traditionally market-led Western rivals to Beijing’s REE empire is China’s use of state resources to strategically build and control the industry’s entire ecosystem, from the REE mining-to-processing value chain to the manufacturing of magnets, electric vehicles, and consumer technology. This has provided Beijing with a powerful card for geoeconomic leverage. Non-Chinese firms also argue Beijing uses monopoly power to disincentivize new entry by foreign competitors.

Responding to China’s REE strategy

The United States

The US has taken many actions to build international partnerships while also aiming to expand domestic output of REEs to diversify supply. In 2022, the Biden administration led the development of the Mineral Security Partnership (MSP), involving 14 countries (including Australia) working toward the goal of "accelerating the development of diverse critical minerals supply chains in cooperation with industry and other governments". Other Biden-era measures include domestic funding for critical minerals through the Inflation Reduction Act and bilateral collaborations such as the Australia-United States Climate, Critical Minerals, and Clean Energy Transformation Compact. More recently, the Trump administration signed an executive order for boosting domestic mineral production, and the US-Ukraine Resources Agreement that provides the US preferential access to Ukrainian critical minerals.

The European Union

Published in 2023, the EU's Economic Security Strategy seeks to bring coherence to EU responses to a more hostile global economic environment by guiding a common EU response to issues surrounding the resilience of supply chains and critical infrastructure. China’s dominance in critical minerals is at the heart of this strategy. Accordingly, the EU’s 2024 Critical Raw Materials Act sets benchmarks for de-risking EU minerals supply by 2030. The act includes minimum targets for EU-located extraction, processing, recycled minerals, and annual consumption of strategic raw materials from a single third country. These EU policies imply opportunities for Australian mineral exports, while the 2024 Australia-EU Memorandum of Understanding on Sustainable Critical and Strategic Minerals aims to facilitate business-to-business links, ensure high environmental, social, and governance standards, and promote fair competition.

Australia

While Canberra has not yet formulated an explicit economic security policy paradigm, the federal government has been making clear moves in that direction. In 2024, the Labor government announced a major new industrial policy – the Future Made in Australia Act – marking a new era of state-led economic policy for an otherwise highly liberal and market-led economy. The government has identified critical minerals as a sector where Australia can build on existing comparative advantages in resource exploitation by moving downstream into the processing of minerals. It is crucial that Canberra’s REE strategy fully leverages US and EU geoeconomic policies aimed at the derisking of global REE supply. Combined, the EU and US account for 26% of global value-add manufacturing, offering large end-user markets for processed REEs.

Australia’s opportunity: Geology and geopolitics

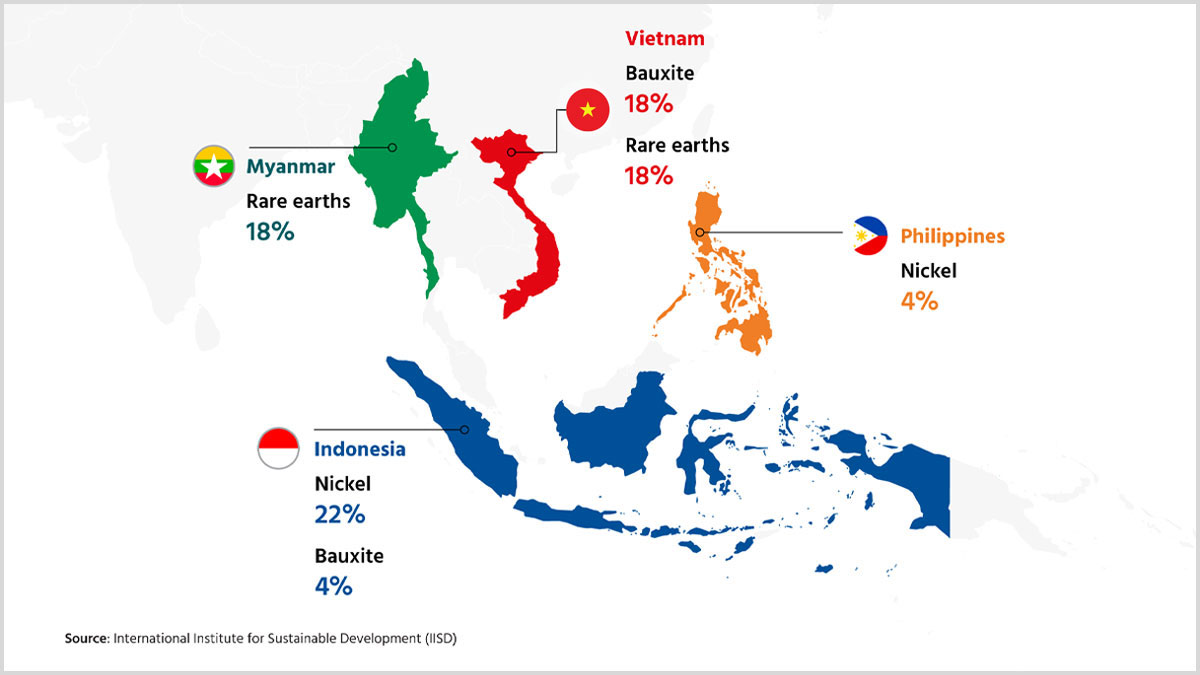

Australia has proven resource sector expertise as well as the geological endowment needed to become a global power in REEs. According to Geoscience Australia, the country has shown economically viable REE resources of 5,700 kilo tons in 2022, with assessed ‘high potential’ for more, versus global production of 350kts in 2023. Australia meanwhile produced 16kts of unrefined REEs in 2022, most of which is shipped to China for processing. Australia’s current critical minerals strategy, as outlined in the government’s "Critical Minerals Strategy 2023-2030" report, aims to "build sovereign capability in critical minerals processing" and work with "like-minded international partners". Canberra has backed up these goals with major policy initiatives ranging from debt funding packages, equity investment, tax credits, to enhanced foreign investment review screening.

Australia’s first REE processing facility was opened in November 2024 by Australian firm Lynas at its Kalgoorlie facility in Western Australia. Yet this facility only engages in partial processing, creating a mixed rare earth carbonate that Lynas will ship to its Malaysian facility for further processing to produce a rare earth oxide. Rare earth oxides are mid-stream inputs ready for use across advanced manufacturing. Lynas has recently faced political and regulatory risks in Malaysia that threatened the closure of its facility, highlighting the vulnerability of its non-integrated supply chain. Hence, a noteworthy part of Australia’s strategy is to create fully integrated mine-to-oxide processing operations within the country. Two firms – Iluka Resources and Arafura Rare Earths – are critical to this plan.

Key challenges

Australia’s prospective REE derisking champions offer valuable insights into key challenges in breaking China’s lock over the market. First, each firm has received large state-backed capital funding that is crucial to the REE sector. This is because private capital is hesitant to invest in REE projects due to the severe opacity of pricing and the high risk of government interference; both of which make it challenging to forecast future returns or the investment risk profile. Large commercial banks’ risk settings leave little appetite for challenging a Chinese state-backed monopoly, leaving firms with few options for capital beyond China itself.

A second insight into the challenge of breaking the REE monopoly is highlighted at the firm level by the routes to market that Iluka and Arafura are taking. Take Arafura’s approach, which seeks to lock in 80% of its annual output in multi-year offtakes before major construction begins. This derisks the price volatility of NdPr oxide and crucially defangs China’s monopoly power to manipulate prices against new market entrants. In principle, this is a smart risk management approach, yet in practice it is proving to be challenging to secure the targeted offtake level. Consider that Arafura officially announced in 2022 that it expected to make final investment decisions in early 2023. Yet by mid-2025 this has still not occurred, with offtake agreements to date at 66%.

So why are end-users of REE oxides not stepping up to secure non-Chinese supply that would safeguard them against burgeoning geoeconomic supply chain risks? There are at least two answers to this question. First, firms are willing to accept supply risk so that they can continue to access the cheapest possible spot market price – despite this spot price being set by opaque and politically compromised dynamics. Second, most of the offtake customers are based in China, and both Arafura’s and Iluka’s debt arrangements prevent accessing these customers. Both answers spell potential trouble for Arafura’s strategy.

The challenges of eschewing Chinese capital are further sharpened by two alternative Australian examples that have not received any Federal funding, VHM Limited and Peak Rare Earths. As a private firm, VHM does not face any "friend-shoring" conditions on its customer base and has secured binding offtake for 60% of annual output from a single customer, Shenghe Resources, a Chinese partly state-owned entity. VHM is using this as the basis to operationalize its Victorian Goschen project, with production set to begin in 2025. In 2023, Peak Rare Earths signed an offtake agreement for up to 100% of its Ngualla project in Tanzania, again with Shenghe Resources, providing the certainty needed to access capital to become operational. These examples highlight the market power and centrality of Chinese capital and offtake demand in the REE value chain.

Steps in the right direction, but derisking challenges remain

Industrial policies designed to shape the commercial decisions of private capital in strategically favorable directions are becoming mainstream in the traditionally market-led advanced economies. However, for these efforts to be successful, policymakers will need to conceptualize commercial ecosystems in whole rather than supply chains in parts. Ultimately, the REE sector is becoming a prime case study for whether liberal market economies can successfully implement economic security policy in our new geoeconomic world order.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Naoise McDonagh

Naoise publishes original research on international business and trade issues, including how domestic regulation, international trade agreements and geopolitics impact the international business environment. In addition, he teaches courses on international business at the undergraduate and postgraduate levels in ECU's School of Business and Law.

Have any feedback on this article?

Related Articles